Manufacturing industry growth is expected to see an upturn during 2025 after a tough 2024 according to an Interact Analysis report.

Global manufacturing insights

- The global manufacturing industry is expected to have a tough 2024, but the landing will be a soft one and a rebound is expected for 2025.

- Not all manufacturing sectors are being affected the same way and the same is true regionally. All sectors were affected by COVID-19, but the impact is not equal.

There are few indicators of a manufacturing recovery in any tri-region at present, as the global downturn continues to affect output, but relatively speaking it could be worse. A soft landing and signs of recovery are anticipated during 2025, according to the Interact Analysis Manufacturing Output Tracker (MIO).

Our measure of global industry and production machinery data and forecasts indicates despite encouraging noises from some stock markets, our customers becoming more positive, and small increases in purchasing managers’ indexes (PMIs), output still remains low and there are few specific indicators that a general recovery will take place in global manufacturing sector during 2024. Any current optimism may be misplaced as we are not seeing the signs yet that signal the timeframe of recovery, despite overall sentiment improving. In addition, many manufacturing economists are still saying there is likely to be a recession.

However, despite little evidence of the current manufacturing downturn abating in the short term, the downturn is not expected to be as bad as previous dips, and longer-term prospects for production look much rosier. The forecast is largely holding steady and a recovery is predicted partway through 2025, with order intakes set to improve towards the end of the year.

Global events present a sobering challenge in 2024

In his introduction to the February update to the MIO, Adrian Lloyd, Interact Analysis CEO, described 2023 as “a strange year characterized by a variety of structural challenges (notably supply chain disruptions), but one that finished more strongly than expected.”

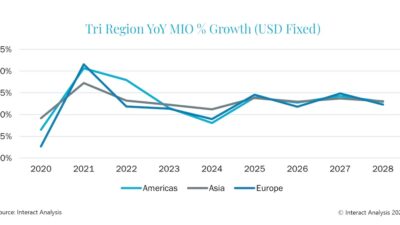

However, he added that growth for 2024 in global manufacturing output is likely to be propped up by 2.4% growth in China (which is below the historic growth trend for the country as economic issues such as the housing market crisis continue to bite). Alongside this, slight contractions are forecast in the manufacturing economies of the Americas (-1.9%) and Europe (-1.0%).

The global economic situation has made a manufacturing slowdown unavoidable, Rising input costs caused by higher inflation have led to interest rate rises that have made businesses more hesitant to invest and have constrained consumer spending. Lenders are becoming more risk-averse and many companies have gone though, or are going through a period of destocking that has seen them using backlogs and running down inventory. Low inventory levels will in time lead to increased activity and we expect order intakes to improve towards 2025.

Furthermore, global events, such as the Hamas/Israel and Ukraine/Russia wars continue to cast a shadow. It is not clear from a forecast perspective what effect the Hamas/Israel conflict will have on the global economy at this time, although there is a risk of escalation. Our thoughts remain with all those affected.

The overall picture differs by sector

Our analysts report a brighter outlook in sectors including robotics, logistics and warehouse automation. The outlook for 2024 shows predicted growth of 20-30% within the mobile robots market, despite the larger industrial segment struggling, and the warehouse industry is showing some signs of recovery after a tough 2023.

Meanwhile, the semiconductor industry appears to be out of step with manufacturing as a whole when it comes to downturns and is forecast a bumper year of double-digit output growth, fuelled by the CHIPS and Inflation Reduction Acts in the US, and current enthusiasm for AI.

The outlook for commercial vehicles is less positive, particularly in off-highway, due to a bad year for agricultural vehicles and a slowdown in construction, while on-highway looks stronger and closer to a flat year. Machinery is also struggling to recover, with high inflation and interest rates dampening incentives to invest following a slow 2023.

Final thoughts

2024 is expected to be a difficult year for most regions, with no territory showing clear signs of recovery. However, the severity of the trough is quite mild for most regions. Key territories such as the US and Germany are expected to shrink around half as much compared with the height of the pandemic. The current slowdown was unavoidable as high inflation rates and subsequent interest rate rises introduced to dampen it continue to bite and drive down demand. However, the landing looks as though it will be soft and take place next year.

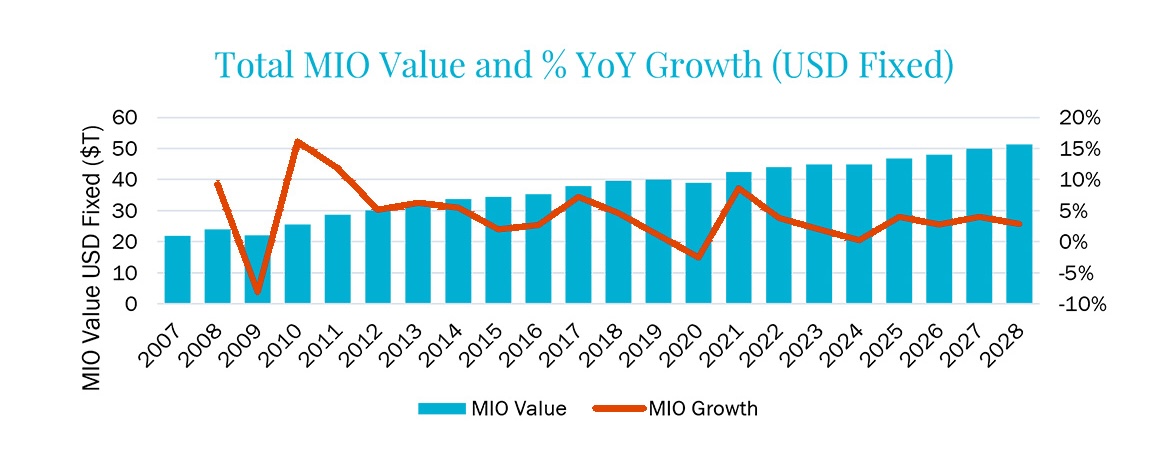

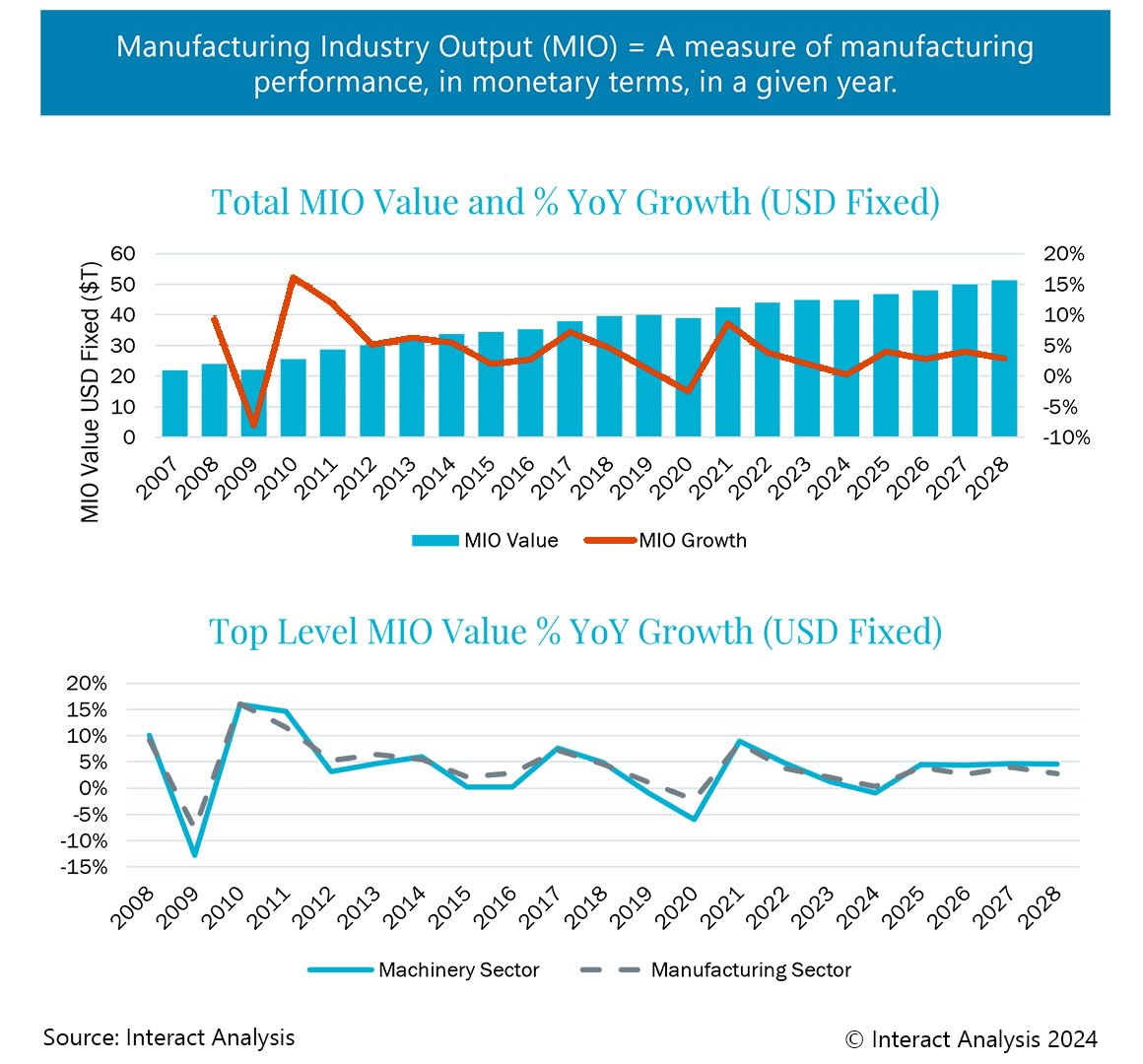

What we can be sure of is that no one knows at present exactly when the turning point for manufacturing will be, so we will be watching closely to see what the data tells us and what happens on the global stage. Manufacturing is cyclical and we currently predict a CAGR of 3.32% between 2023 and 2028. There are no huge supply side issues affecting the industry at present and prospects appear relatively strong for growth in the longer term.

– Interact Analysis is a CFE Media and Technology content partner.