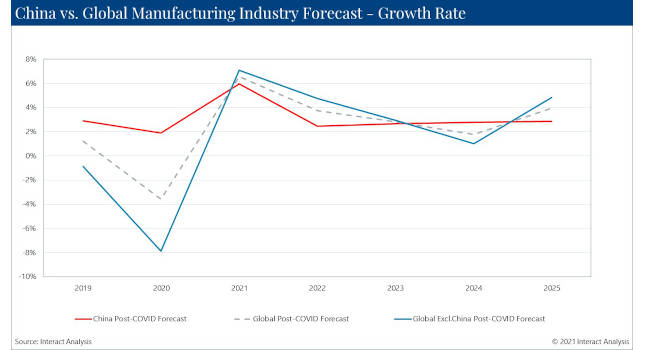

While manufacturing in China did well in 2020, Interact Analysis reports its growth will lag behind other countries in 2021.

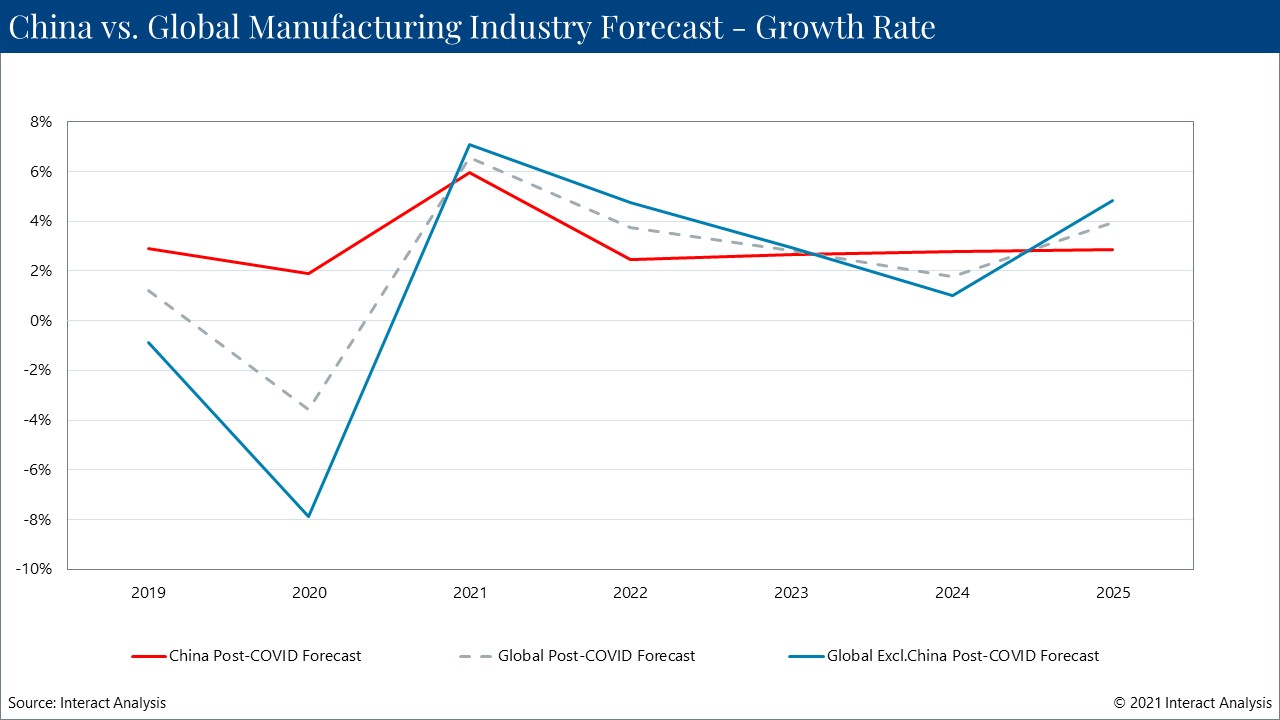

Chinese manufacturing did comparatively well in 2020 in spite of the COVID-19 pandemic. All indicators point to continued growth, though it will be uneven. But China will eventually trail behind other countries in terms of growth during 2021. This is simply because the country is bouncing back from a higher base, while other countries are likely to belatedly put on a growth spurt, having had their economies hammered far harder at the height of the pandemic.

The shock of COVID-19 saw the country experience a -6.8% contraction in GDP in the first quarter of 2020 (according to the National Bureau of Statistics of China), but strong measures taken against the spread of the virus brought it under control and stabilized production. By the end of 2020, China was the only major region able to report a positive rate of manufacturing growth, standing at +1.9%, outpacing all other major economies, some of which were destined to falter for a longer time, and many of which are still struggling.

The macro-economic picture directly impacts manufacturing

The challenge now for the Chinese government is to stabilize their growth rate, keeping major macro indicators within a reasonable range in order to avoid fluctuations in employment rates and prices. It’s going to be a challenge, and to respond effectively to it, the government has come up with the concept of ‘cross-cycle adjustment’, which has the aim of evening out the effects of the huge fluctuations in China’s economic performance which started with the onset of the pandemic and are predicted to run into 2022. That -6.8% contraction in GDP in Q1 of 2020 gave rise to reciprocal pressure leading to +18.3% growth in Q1 of 2021. Then in Q2 of 2021, the growth rate went down to below 8% as orders dried up following the glut in Q1. The figure for Q1 of 2022 is projected to be nowhere near that of Q1 2021. The pressure is on and the challenge for the government is to formulate macroeconomic policies which smooth the ride. As a consequence of this instability we have reduced our predicted growth rate for China’s manufacturing industry in 2021 from 6.4 to 5.9%.

In spite of problems, most industries grew by >10% in the first half

The data presented in the chart below shows that most industries experienced >10% year-on-year growth in the first half of 2021. Certain sectors, such as medicines, fabricated metal products and electric machinery and equipment saw increases of more than 20%.

But there’s good news and bad. Whilst in June the added value of manufacturing industries above designated size (an official Chinese term referring to industries with annual revenues of $3.3m or more) saw a year-on-year increase of 8.3%, there was a fall in added value on a month-on-month basis for the five consecutive months leading up to June. This manufacturing decline has been caused by a slowdown in demand, with the new order index, for example, falling by 0.6 percentage points between June and July. Meanwhile, recent rises in raw material costs and delivery times, along with worries about the delta variant, mean that manufacturing will be under major pressure in the last part of the year.

But on the positive side, investment in industry has returned to and in some cases exceeded pre-COVID-19 levels, increasing by 20.4% in H1 2021, compared with -11.7% in H1 2020, suggesting that enthusiasm for investing in Chinese manufacturing may even be exceeding what it was pre-COVID.

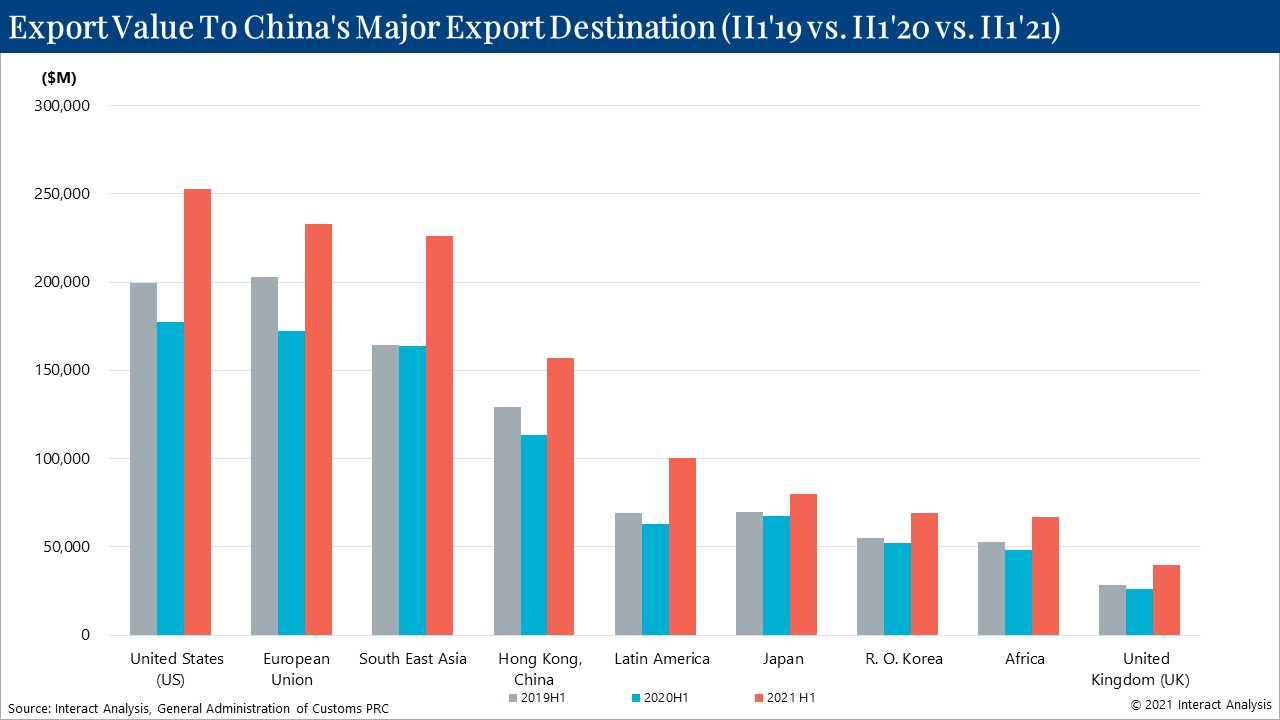

Growth of >20% for exports in 2nd quarter of 2021

March 2020 saw the lowest growth rate for China’s exports since 2019. That figure, -6.6% (year-on-year) was turned into a massive +155% by February 2021. This partly reflected the low base value in February 2020 but was also a result of the continued COVID-induced disruption of supply chains across the globe, obliging countries to import goods from China. China’s export growth has dropped from its February peak and continues at a rate of over 20%. The proportion of exports to different destinations has changed little compared with 2020, with the US, EU, Southeast Asia, Hong Kong, and Latin America being the top five.

The value of exports in the first half of 2021 to all of China’s main export destinations exceeded values for the corresponding period in 2019, with export values to the top four exceeding 100 billion yuan.

Even doing well has its downsides

We saw earlier that China was the only region to record a positive growth rate in manufacturing for 2020 of +1.9%, whilst the rest of the world registered negative growth, averaging -7.9%. We expect China’s manufacturing output in 2021 to return to the level we were predicting pre-pandemic. This is swift compared to other countries that will have to wait until the end of 2021 or going into 2022. This is, also, interestingly, going to mean that as recovery for other countries gets underway, we will for the first time since we started tracking industrial output see China’s manufacturing output lagging below the global average.

– This originally appeared on Interact Analysis’ website. Interact Analysis is a CFE Media content partner.