SEMI’s latest World Fab Forecast report projects a 2% YoY increase in global front-end fab equipment spending.

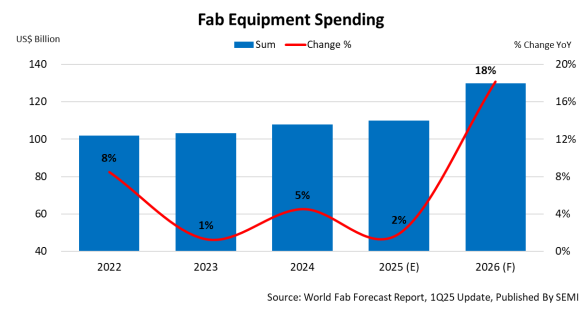

Global fab equipment spending for front-end facilities in 2025 is expected to rise by 2% year-over-year (YoY) to $110 billion, continuing a growth trend since 2020, according to SEMI’s latest World Fab Forecast report. A recent industry report also highlights semiconductor manufacturing growth trends in Q3 2024.

Fab equipment spending is expected to rise by 18% in 2026, reaching $130 billion. This increase is driven by demand in high-performance computing (HPC) and memory sectors for data center expansion, as well as the growing use of artificial intelligence (AI), which is raising silicon requirements for edge devices.

“The global semiconductor industry’s investments in fab equipment have been edging up for six straight years, and spending is poised to see a strong 18% increase in 2026 as production ramps to meet booming AI-related chip demand,” said Ajit Manocha, SEMI president and CEO. “This forecasted capex growth signals an urgent need for intensified workforce development initiatives throughout 2025 and 2026 to deliver skilled workers necessary for the approximately 50 new fabs expected to come online during these two years.”

Logic and micro segment lead semiconductor industry expansion

The logic and micro segment is expected to drive growth in fab investments. This growth is supported by investments in the 2-nanometer process and backside power delivery technology, which are set to enter production by 2026. Investments in the segment are projected to increase 11% to $52 billion in 2025, and 14% to $59 billion in 2026.

Overall memory segment spending is expected to rise over the next two years, increasing 2% to $32 billion in 2025 and 27% in 2026. DRAM investments are projected to decline by 6% year-over-year, totaling to $21 billion in 2025 before rising 19% to $25 billion in 2026. NAND spending is forecast to grow 54% year-over-year to $10 billion in 2025 and 47% to $15 billion in 2026.

China continues to lead in regional fab equipment spending

After reaching $50 billion in 2024, China is projected to remain the largest market for global semiconductor equipment spending, with an estimated $38 billion in 2025, a 24% decline from the previous year. Spending is expected to fall another 5% to $36 billion in 2026.

As AI adoption increases, Korean chipmakers plan to increase investments in equipment for expanding capacity and upgrading technology. This is expected to make the region the second-largest spending through 2026. Korea’s semiconductor investment is projected to rise 29% to $21.5 billion in 2025 and 26% to $27 billion in 2026.

Taiwan is expected to be the third-largest spender on semiconductor equipment as Taiwanese chipmakers plan to strengthen their position in advanced technology and production. Taiwan is projected to invest $21 billion in 2025 and $24.5 billion in 2026 to support the increasing demand for AI applications in cloud services and edge devices.

The Americas region is expected to be the fourth-largest spender, with investments reaching $14 billion in 2025 and $20 billion in 2026. Japan, Europe and the Middle East and Southeast Asia are expected to spend $14 billion, $9 billion, and $4 billion in 2025, and $11 billion, $7 billion, and $4 billion in 2026.

The March update of the SEMI World Fab Forecast report includes approximately 1,500 facilities and lines worldwide. Off these, 156 are set to begin operation in 2025 or later.

Download a sample of the SEMI World Fab Forecast report.

For details about SEMI reports on other semiconductor sectors, visit SEMI Market Data.

Edited by Puja Mitra, WTWH Media, for Control Engineering, from a SEMI news release.