Interact Analysis quarterly Manufacturing Industry Output (MIO) Tracker report forecasts growth of 0.6% for 2024, with stronger growth expected in 2025 and beyond.

Learning Objectives

- Marginal growth of 0.6% is predicted for manufacturing output in 2024.

- The Asia-Pacific region will play a pivotal role in manufacturing output growth for 2024.

- Machine manufacturing will prove challenging.

Global manufacturing insights

- While global manufacturing output is expected to grow by 0.6% in 2024, a more positive outlook is forecast in 2025 and beyond.

- Germany’s manufacturing economy will continue to struggle throughout 2024.

- South Korea, Singapore and Taiwan are leading the global recovery in the semiconductor.

Despite short-term challenges, the long-term outlook for the global manufacturing industry is positive, according to market intelligence firm Interact Analysis. The company’s latest quarterly Manufacturing Industry Output (MIO) Tracker report forecasts marginal growth of 0.6% for 2024, with stronger growth expected in 2025 and beyond. However, the growth forecast for China’s manufacturing output has been revised down slightly to 2.3% for 2024, the company said in a Sept. 9 statement.

European manufacturing performance

Europe as a whole is bracing for a difficult year in 2024, with the manufacturing sector expected to face significant downturns across multiple key economies. The region is grappling with the aftereffects of energy crises, supply chain disruptions and the ongoing economic fallout from geopolitical tensions, particularly the war in Ukraine. As a result, Europe’s manufacturing output at a country-level is projected to either stagnate or decline, making it one of the weakest performing regions globally. The anticipated downturn highlights the region’s vulnerability to external shocks and underscores the urgent need for strategic investments in energy independence and industrial modernization to ensure longer-term resilience.

Asia-Pacific manufacturing performance summary

The Asia-Pacific region, particularly South Korea, Singapore and Taiwan, are poised to play pivotal roles in the global recovery for the manufacturing sector. Following on from a challenging 2023 marked by supply chain disruptions and reduced demand, these three countries are expected to experience a significant resurgence as the semiconductor industry regains momentum. Meanwhile, China remains, as expected, on a growth trajectory, albeit with its economic expansion slowing down.

U.S. manufacturing performance summary

In contrast, the United States, although facing a slowdown, is not expected to experience as severe a downturn as the European manufacturing sector. This is in part due to a high amount of investment in infrastructure. Political changes, however, like the upcoming presidential election, may affect the country’s growth prospects.

Global manufacturing: China, machinery, advanced manufacturing, automation

While the global manufacturing industry is projected to see a slight increase in output, the picture changes significantly when China is excluded from the analysis. Without China, global manufacturing output is expected to decline by 0.9% in 2024, underscoring the critical role China plays in the global manufacturing ecosystem.

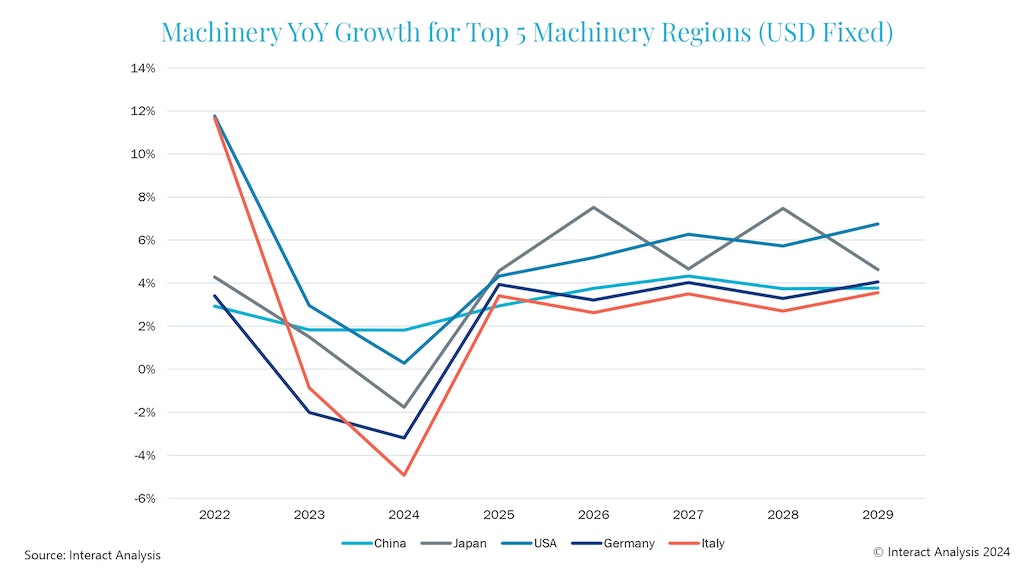

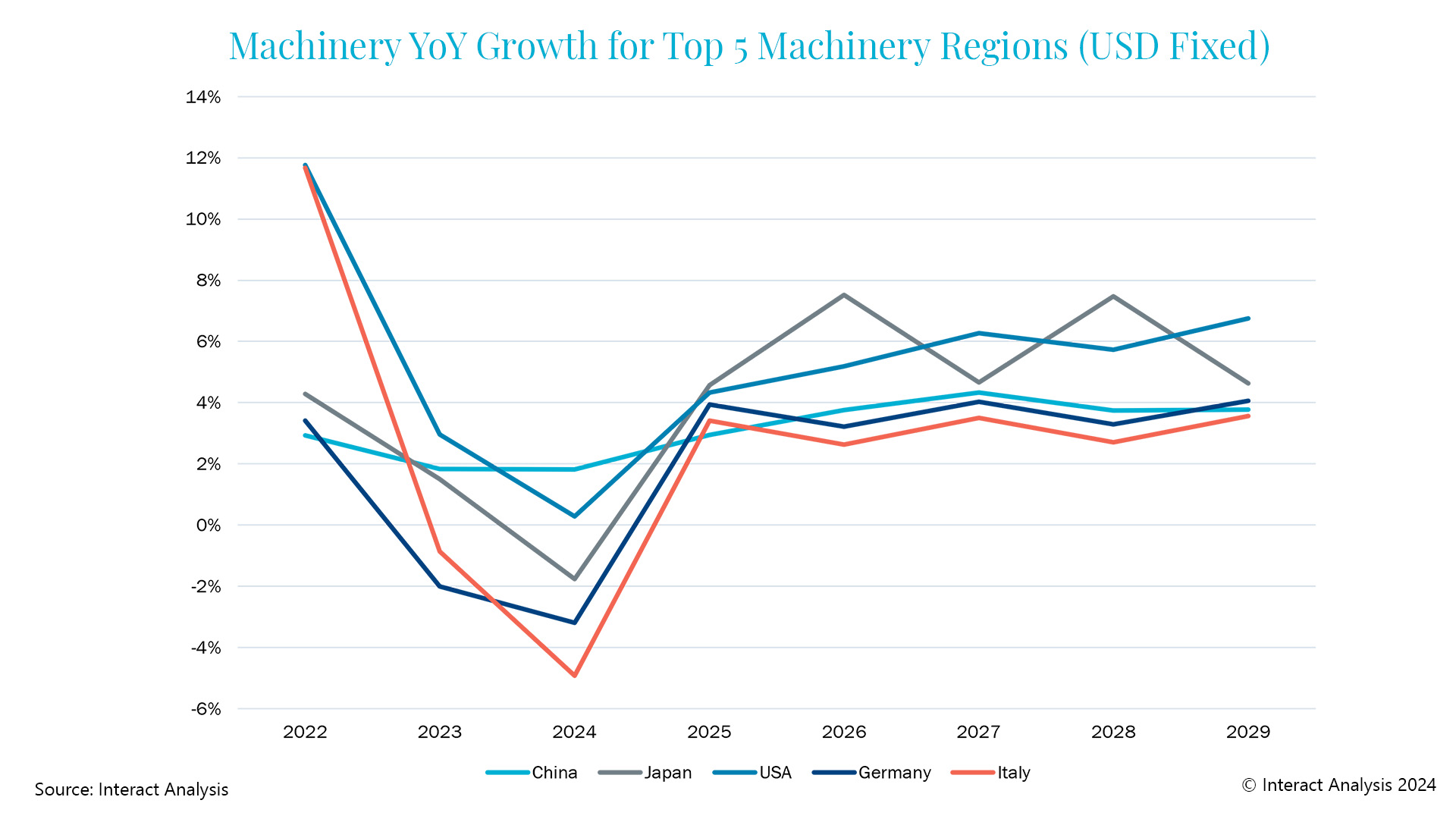

The machinery manufacturing sector is predicted to have a more challenging year in 2024. In Europe, particularly in Germany and Italy – two of the region’s largest machinery producers – the sector is forecast to stagnate or even decline. This downturn is driven by several factors, including increased competition from lower-cost producers in Eastern Europe and Asia, high interest rates and inflation stifling investment and the ongoing energy crisis in Germany (a result of the reliance on Russian gas and the ongoing war in Ukraine), which has led to higher production costs. (The figure shows a graph of the top five machinery regions’ year-over-year percentage growth from 2022 projected through 2028.)

Despite these challenges facing European sectors, some regions, especially in Asia, may see better performance due to investments in more advanced manufacturing technologies and automation, which are expected to bolster productivity and production for machinery sectors.

Adrian Lloyd is CEO at Interact Analysis, a Control Engineering content partner; edited by Judy Pinsel, Control Engineering, WTWH Media.

ONLINE

Also from Interact Analysis, see these manufacturing predictions reported by Control Engineering in February.